.jpg&w=3840&q=100)

Market

Insights

Reports delivered globally, covering a wide range of industries and sectors.

Clients who trust our expertise and rely on our insights for business decisions.

Managed Reports, ensuring seamless updates and premium service.

Satisfied Customers, committed to delivering exceptional value and quality.

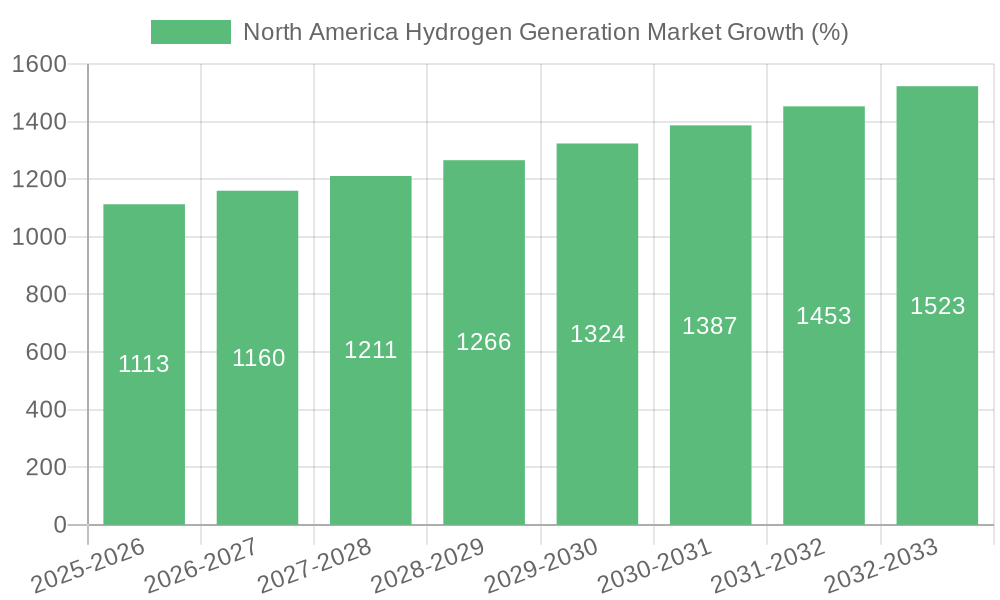

North America Hydrogen Generation Market 2025-2033 Overview: Trends, Dynamics, and Growth Opportunities

North America Hydrogen Generation Market by Delivery Mode (Captive, Merchant), by Process (Steam Reformer, Electrolysis, Others), by Application (Petroleum Refinery, Chemical, Metal, Others), by North America (U.S., Canada) Forecast 2025-2033

North America Hydrogen Generation Market 2025-2033 Overview: Trends, Dynamics, and Growth Opportunities

Key Insights

The North American hydrogen generation market, valued at approximately $18.5 billion in 2025, is projected to experience robust growth, driven by increasing demand from the petroleum refinery, chemical, and metal sectors. A compound annual growth rate (CAGR) of 5.8% from 2025 to 2033 indicates a significant expansion over the forecast period. This growth is fueled by several factors. The burgeoning renewable energy sector is pushing for hydrogen as a clean energy carrier, particularly in green hydrogen production via electrolysis. Stringent environmental regulations aiming to reduce carbon emissions are also incentivizing the shift towards hydrogen, especially in heavy industries where decarbonization remains a major challenge. Furthermore, advancements in hydrogen generation technologies, such as improved steam methane reforming and the rising cost-competitiveness of electrolysis, are making hydrogen production more efficient and economically viable. The market is segmented by delivery mode (captive and merchant), process (steam reforming, electrolysis, and others), and application (petroleum refinery, chemical, metal, and others). The captive segment, where hydrogen is produced and used within the same facility, is expected to dominate, reflecting the integration of hydrogen production within existing industrial processes. However, the merchant segment, encompassing the sale and distribution of hydrogen, is projected to witness substantial growth fueled by increasing demand from various end-use sectors. The US and Canada are major contributors to the North American market, primarily due to their well-established industrial bases and government support for clean energy initiatives.

The competitive landscape includes major players like Air Products and Chemicals, Linde plc, and Plug Power Inc., each bringing its unique strengths and technological advancements to the table. The market's growth trajectory is poised for further acceleration as technological breakthroughs continue, governmental policies become more supportive, and industrial demand increases. However, challenges such as high capital investment costs associated with hydrogen infrastructure development and fluctuations in feedstock prices (natural gas for steam reforming) could pose temporary limitations. Overall, the North American hydrogen generation market presents a significant investment opportunity with considerable potential for long-term growth and positive environmental impact, creating a sustainable and increasingly significant contribution to the energy transition.

North America Hydrogen Generation Market Concentration & Characteristics

The North American hydrogen generation market is characterized by a moderate level of concentration, with a few large multinational corporations holding significant market share. Air Products, Linde, and Plug Power are prominent examples, alongside several regional players. Innovation is primarily focused on improving the efficiency and reducing the cost of electrolysis, particularly green hydrogen production fueled by renewable energy sources. Significant advancements are also being made in hydrogen storage and transportation technologies.

- Concentration Areas: Primarily concentrated in regions with significant industrial activity and access to renewable energy resources, such as Texas, California, and the Midwest in the US, and Ontario in Canada.

- Characteristics of Innovation: Focus on cost reduction of green hydrogen via improved electrolysis, development of advanced materials for electrolyzers, and exploration of innovative hydrogen storage and transport solutions.

- Impact of Regulations: Government incentives and policies promoting clean energy, including tax credits and grants for hydrogen production, are driving market growth. Stringent emission regulations are also pushing industries to adopt hydrogen as a cleaner fuel alternative.

- Product Substitutes: Natural gas remains a significant competitor, especially for grey hydrogen production. However, increasing environmental concerns and government regulations are gradually shifting the preference towards green and blue hydrogen.

- End User Concentration: The largest consumers are the petroleum refinery, chemical, and metal industries, representing substantial demand.

- Level of M&A: The market has witnessed a moderate level of mergers and acquisitions activity, driven by companies seeking to expand their production capacity, enhance their technology portfolio, and secure access to renewable energy resources. This activity is expected to increase in the coming years as the market matures.

North America Hydrogen Generation Market Trends

The North American hydrogen generation market is experiencing rapid growth driven by several key trends. The increasing adoption of renewable energy sources, particularly wind and solar, is significantly impacting hydrogen production. The shift toward green hydrogen, produced through electrolysis powered by renewable energy, is gaining significant traction, driven by environmental concerns and government support for clean energy initiatives. Furthermore, technological advancements in electrolysis are improving efficiency and reducing production costs, making hydrogen a more competitive energy source. The development of hydrogen infrastructure, including pipelines and storage facilities, is another crucial trend supporting market expansion. Several governmental policies and incentives are being introduced to catalyze the market's growth by offering tax credits, subsidies, and grants. Industrial sectors, notably petroleum refineries, chemical manufacturers, and steel producers, are increasingly adopting hydrogen for various processes, primarily for decarbonization purposes. The rising demand for hydrogen in transportation, both in fuel cell electric vehicles and as a fuel for heavy-duty vehicles, is also creating significant opportunities. Finally, growing private and public investments are contributing significantly to the sector's progress. This includes substantial investments in large-scale green hydrogen production facilities, research and development projects, and infrastructure development.

Key Region or Country & Segment to Dominate the Market

The Electrolysis segment is poised to dominate the North American hydrogen generation market. This is primarily due to the increasing emphasis on green hydrogen production, driven by environmental concerns and government policies. Electrolysis, using renewable energy sources, is pivotal in producing green hydrogen, a significantly cleaner alternative compared to traditional steam methane reforming.

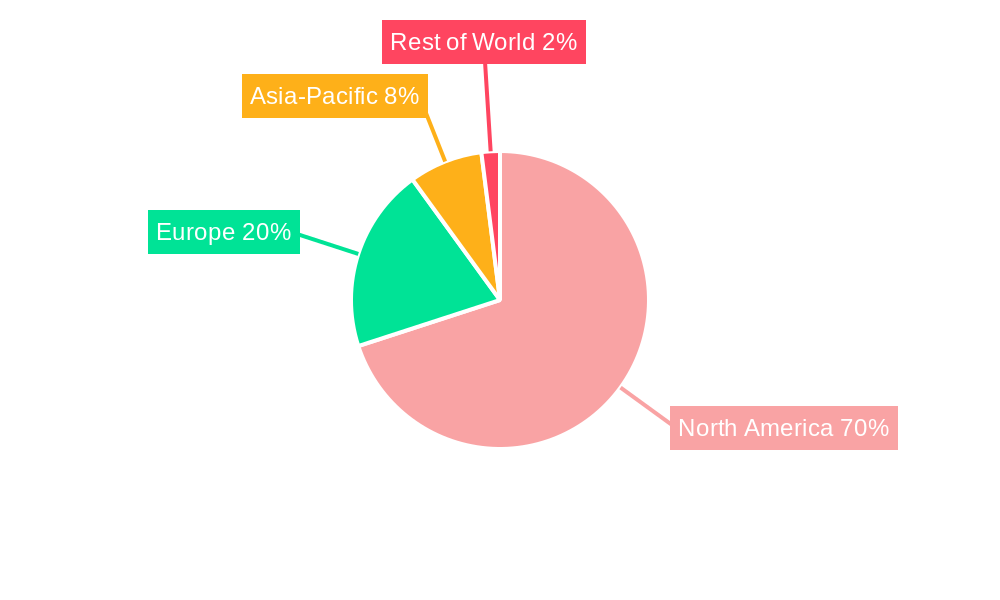

- Dominant Region: The United States will likely remain the dominant market due to its larger industrial base, significant investments in renewable energy, and supportive government policies. Texas, in particular, is emerging as a major production hub due to its abundant wind and solar resources.

- Dominant Segment (Process): Electrolysis, driven by the growing adoption of green hydrogen and supportive government initiatives. The segment will witness robust growth fueled by advancements in technology leading to improved efficiency and lower costs.

- Dominant Segment (Delivery Mode): The Merchant segment is anticipated to experience faster growth. While captive generation remains dominant for many industrial players, the merchant model's flexibility in offering hydrogen across various sectors and geographical locations offers substantial potential.

The growth within the electrolysis segment is underpinned by significant investments in large-scale green hydrogen projects, along with the ongoing development of more efficient and cost-effective electrolyzer technologies. Simultaneously, supportive government policies and increasing demand from various industrial sectors will continue to fuel market expansion.

North America Hydrogen Generation Market Product Insights Report Coverage & Deliverables

This report provides comprehensive insights into the North American hydrogen generation market, encompassing detailed analysis of various segments, including delivery mode (captive and merchant), production processes (steam reforming, electrolysis, and others), and applications across different industrial sectors. It offers market sizing, segmentation, regional breakdowns, and detailed competitive landscape analysis, including key players' profiles and market share estimations. The report also assesses the impact of key trends, driving forces, challenges, and regulatory landscapes, providing valuable insights into the market's future trajectory.

North America Hydrogen Generation Market Analysis

The North American hydrogen generation market is projected to reach a valuation of approximately $50 billion by 2030, exhibiting a significant compound annual growth rate (CAGR) of over 15% during the forecast period. This substantial growth is fueled by the increasing demand for clean energy solutions, coupled with government incentives promoting hydrogen as a sustainable fuel source. The market share is currently dominated by grey hydrogen production from steam reforming, but this is expected to shift substantially towards green hydrogen generated through electrolysis in the coming years. The market's value will be driven by increasing adoption of green hydrogen across various industries. This includes petroleum refineries adopting hydrogen for hydrocracking and hydrotreating, the chemical industry using hydrogen in ammonia synthesis and methanol production, and the metal industry for steel production and other metallurgical applications.

North America Hydrogen Generation Market Regional Insights

- North America

- U.S.

- Delivery Mode: Captive, Merchant

- Process: Steam Reformer, Electrolysis, Others

- Application: Petroleum Refinery, Chemical, Metal, Others

- Canada

- Delivery Mode: Captive, Merchant

- Process: Steam Reformer, Electrolysis, Others

- Application: Petroleum Refinery, Chemical, Metal, Others

- U.S.

Driving Forces: What's Propelling the North America Hydrogen Generation Market

The North American hydrogen generation market is experiencing rapid growth due to several key driving factors: increasing environmental concerns and stricter emission regulations pushing for cleaner fuel alternatives; substantial government support and investments through tax credits, subsidies, and research funding; technological advancements in electrolysis, leading to higher efficiency and lower costs; growing demand from diverse industrial sectors for hydrogen in various applications; and the emergence of hydrogen as a viable energy carrier in the transportation sector.

Challenges and Restraints in North America Hydrogen Generation Market

Significant challenges exist, including the high initial investment costs associated with hydrogen production facilities and infrastructure; the lack of widespread infrastructure for hydrogen storage, transportation, and distribution; the intermittent nature of renewable energy sources used for green hydrogen production; and the need for continued technological advancements to further reduce production costs and improve efficiency.

Emerging Trends in North America Hydrogen Generation Market

The market is witnessing several emerging trends: a notable rise in the use of Power-to-X technologies to produce hydrogen and other synthetic fuels from renewable energy; increasing integration of hydrogen generation with carbon capture and storage (CCS) technologies to produce blue hydrogen; the exploration of diverse hydrogen storage methods, including underground storage and the use of advanced materials; and a growing focus on the development of hydrogen fuel cell technology for transportation and other applications.

North America Hydrogen Generation Industry News

- December 2022: Air Products and The AES Corporation announced a USD 4 billion investment in a green hydrogen production plant in Texas.

- April 2024: First State Hydrogen, Inc. partnered with Siemens Energy for a green hydrogen production facility design study in the Mid-Atlantic region.

Leading Players in the North America Hydrogen Generation Market

- Air Products and Chemicals, Inc.

- Ballard Power Systems

- CALORIC

- CF Industries

- Cummins Inc.

- Hexagon Composites ASA

- Iwatani Corporation

- ITM Power plc

- Linde plc

- Messer

- NUVERA FUEL CELLS, LLC

- Nel ASA

- Plug Power Inc.

- RESONAC HOLDINGS CORPORATION

- Siemens Energy AG

North America Hydrogen Generation Market Segmentation

-

1. Delivery Mode

- 1.1. Captive

- 1.2. Merchant

-

2. Process

- 2.1. Steam Reformer

- 2.2. Electrolysis

- 2.3. Others

-

3. Application

- 3.1. Petroleum Refinery

- 3.2. Chemical

- 3.3. Metal

- 3.4. Others

North America Hydrogen Generation Market Segmentation By Geography

-

1. North America

- 1.1. U.S.

- 1.2. Canada

North America Hydrogen Generation Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.8% from 2019-2033 |

| Segmentation |

|

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Rising Government Investments and Funding

- 3.2.2 Growing Renewable Energy Integration

- 3.2.3 Rising Technological Advancements and Innovation

- 3.3. Market Restrains

- 3.3.1. High initial capital investment

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Hydrogen Generation Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Delivery Mode

- 5.1.1. Captive

- 5.1.2. Merchant

- 5.2. Market Analysis, Insights and Forecast - by Process

- 5.2.1. Steam Reformer

- 5.2.2. Electrolysis

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Petroleum Refinery

- 5.3.2. Chemical

- 5.3.3. Metal

- 5.3.4. Others

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Delivery Mode

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Air Products and Chemicals Inc.

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Ballard Power Systems

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 CALORIC

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 CF Industries

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Cummins Inc.

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Hexagon Composites ASA

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Iwatani Corporation

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 ITM Power plc

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Linde plc

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Messer

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 NUVERA FUEL CELLS LLC

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Nel ASA

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 Plug Power Inc.

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.14 RESONAC HOLDINGS CORPORATION

- 6.2.14.1. Overview

- 6.2.14.2. Products

- 6.2.14.3. SWOT Analysis

- 6.2.14.4. Recent Developments

- 6.2.14.5. Financials (Based on Availability)

- 6.2.15 Siemens Energy AG

- 6.2.15.1. Overview

- 6.2.15.2. Products

- 6.2.15.3. SWOT Analysis

- 6.2.15.4. Recent Developments

- 6.2.15.5. Financials (Based on Availability)

- 6.2.1 Air Products and Chemicals Inc.

- Figure 1: North America Hydrogen Generation Market Revenue Breakdown (Billion, %) by Product 2024 & 2032

- Figure 2: North America Hydrogen Generation Market Share (%) by Company 2024

- Table 1: North America Hydrogen Generation Market Revenue Billion Forecast, by Region 2019 & 2032

- Table 2: North America Hydrogen Generation Market Revenue Billion Forecast, by Delivery Mode 2019 & 2032

- Table 3: North America Hydrogen Generation Market Revenue Billion Forecast, by Process 2019 & 2032

- Table 4: North America Hydrogen Generation Market Revenue Billion Forecast, by Application 2019 & 2032

- Table 5: North America Hydrogen Generation Market Revenue Billion Forecast, by Region 2019 & 2032

- Table 6: North America Hydrogen Generation Market Revenue Billion Forecast, by Delivery Mode 2019 & 2032

- Table 7: North America Hydrogen Generation Market Revenue Billion Forecast, by Process 2019 & 2032

- Table 8: North America Hydrogen Generation Market Revenue Billion Forecast, by Application 2019 & 2032

- Table 9: North America Hydrogen Generation Market Revenue Billion Forecast, by Country 2019 & 2032

- Table 10: U.S. North America Hydrogen Generation Market Revenue (Billion) Forecast, by Application 2019 & 2032

- Table 11: Canada North America Hydrogen Generation Market Revenue (Billion) Forecast, by Application 2019 & 2032

STEP 1 - Identification of Relevant Samples Size from Population Database

STEP 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note* : In applicable scenarios

STEP 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

STEP 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

Frequently Asked Questions

Related Reports

See the similar reports

About Market Insights Report

Market Insights Reports offers comprehensive market research reports and analysis, giving businesses important information about their clients, rivals, and sector to help them make well-informed decisions on operations, marketing, and business strategy. We offer a variety of services in addition to market research, data analysis, and strategy planning. In order to find opportunities and learn more about our competitors and the industry at large, we employ competitive analysis. To identify areas for development, we also evaluate our performance against that of our rivals. We can determine the places at which we can offer our clients the most value by performing value chain analysis.

Additionally, clients receive a thorough overview of their industry business environment. We can find trends that help us forecast future possibilities and threats by examining global macroeconomic dynamics and consumer behavior patterns. By analyzing their features and advantages, contrasting them with comparable items on the market, and evaluating both their quantitative and qualitative performance, we comprehensively evaluate our clients' products. This allows us to assist customers in determining how their goods compare to those of their rivals and in creating successful marketing plans. Our group has been successful in gaining a thorough grasp of our clients' requirements and offering them creative solutions. We currently provide services to more than 50 nations in Europe, the Middle East, Africa, Latin America, Asia Pacific, and North America. Because of our global reach, we have been able to establish trusting bonds with our partners and clients in various nations, improving customer service and forging a more cohesive worldwide presence.